Assessing green bond opportunities

Commentary by Kunal Mehta, senior investment specialist, fixed income, and Loubna Moudanib, credit analyst in Vanguard's Fixed Income Group.

Interest in environmental, social and governance (ESG) investing has grown rapidly in recent years as investors increasingly look for ways to mitigate ESG-related risk or effect meaningful change. Fixed income is no exception to this trend, as bonds marketed under a number of ESG labels have proven popular with investors.

These include social bonds, whose proceeds are used to finance or re-finance projects that provide clear social benefits; sustainability-linked bonds, which have financial or structural characteristics that can vary depending on whether the issuer achieves predefined sustainability or ESG objectives; as well as green bonds, which back projects with clear environmental benefits1.

But the rise of these bonds has been accompanied by some confusion around both how to define them and how to analyse their green credentials. The rapidly expanding universe of green bonds in particular has stimulated a great deal of debate and misunderstanding among some investors.

Corporate green bonds now make up around 1.8% of the Bloomberg Barclays Global Aggregate Corporate Bond Index, up from less than 0.4% five years ago2, driven by rising issuance, growing institutional demand and increasing standardisation.

As with any other kind of financial instrument, it’s important for investors in green bonds to understand the risk and performance implications of what they’re investing in.

Expanding opportunity set

The green-bond opportunity set is growing swiftly – research from Morgan Stanley suggests that European green bond issuance during the first quarter of 2021 equates to half of the total issued during the whole of 20203. Governments, for one, are ramping up their issuance of green bonds. In 2020, EU leaders agreed to borrow €750 billion to provide grants and loans to help member states to recover from the Covid-19 pandemic, part of which will take the form of green bonds. Similarly, the UK’s Debt Management Office has announced a green-bond issuance programme in response to the pandemic as well as to boost its sustainable finance program, with plans to issue two “green gilts” in 2021.

Corporate borrowers are following sovereign issuers’ lead, increasing their green bond issuance and taking advantage of the typically lower funding costs of green bonds relative to non-green bonds while boosting their green credentials, allowing them to tap into the growing investor appetite for green bonds.

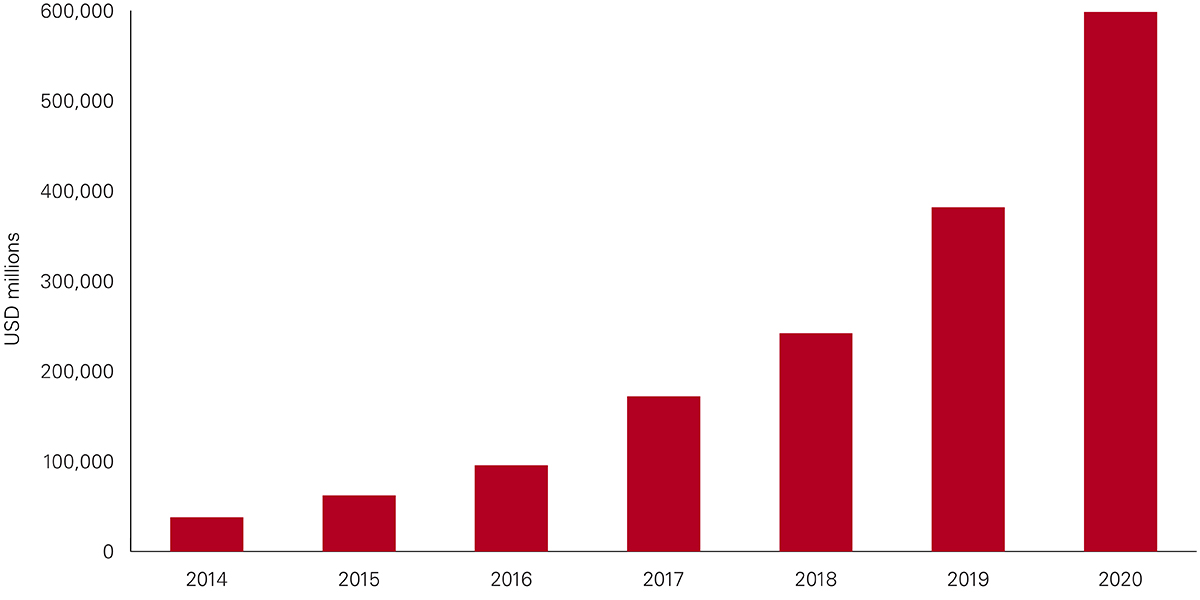

In 2014, Bloomberg Barclays and MSCI introduced a benchmark to represent the green-bond universe, the Bloomberg Barclays MSCI Global Green Bond Index. Initially the benchmark tracked a handful of issuers, limited to development banks and supranational entities, but today it also includes a large number of corporate issuers and the debt the index tracks has risen from $15 billion at inception to around $600 billion today4.

Bloomberg Barclays MSCI Global Green Bond Index size

Source: Bloomberg Barclays, as at 31 December 2020

But while the market for green bonds has grown significantly, how do the returns offered by green bonds compare with their non-green peers?

For new issues, there does appear to be an initial “greenium”—a premium over non-green bonds—as green bonds tend to trade at tighter spreads than conventional bonds. New bond issues are typically priced to include a new-issue premium—that is, an extra yield above that offered by bonds already in the market—to attract investors. As strong investor interest has driven oversubscription in new green issues, the average spread tightening from the initial pricing to issuance for green bonds has been 23 basis points for debt issued in Europe over the past four years, relative to 19 basis points for conventional bonds5. It’s important to note that spreads can vary by sector and issuer.

Average corporate spread compression from initial pricing to issuance – green versus non-green bonds (in basis points)

Source: Bloomberg Barclays, as at 31 March 2021.

However, when you look beyond the spreads at issuance, we have observed no evidence of consistent green-bond outperformance relative to “plain vanilla” bonds. On aggregate, our analysis shows that green bonds performed broadly in line with conventional bonds over the past one- and five-year horizons, on a risk-adjusted basis6.

And based on our analysis of green bonds relative to non-green bonds from the same issuer with otherwise identical characteristics, we have found no strong evidence of a consistent “greenium” which endures beyond issuance7. What’s more, based on the evidence to date, we can’t conclude that green bonds provide better (or worse, for that matter) shock-absorbing properties than conventional bonds in the event of interest-rate hikes, credit downgrades or macroeconomic shocks.

Credit analysis equally important

Green bonds rank “pari passu”—that is, they claim equal seniority—with an issuer’s other bonds in the same structure, and in terms of fundamental credit analysis, credit risk sits at the issuer level and is exactly the same for a green bond as for a non-green bond.

That said, not all green bonds are created equal. Just like conventional bonds, they differ by credit quality, currency, maturity and structure, among other factors, and are subject to the same fundamental analysis. Investors also need to be mindful of the practice of “greenwashing”, whereby some firms may engage in certain behaviours—such as issuing green bonds—motivated more by reputational aims than by environmental goals.

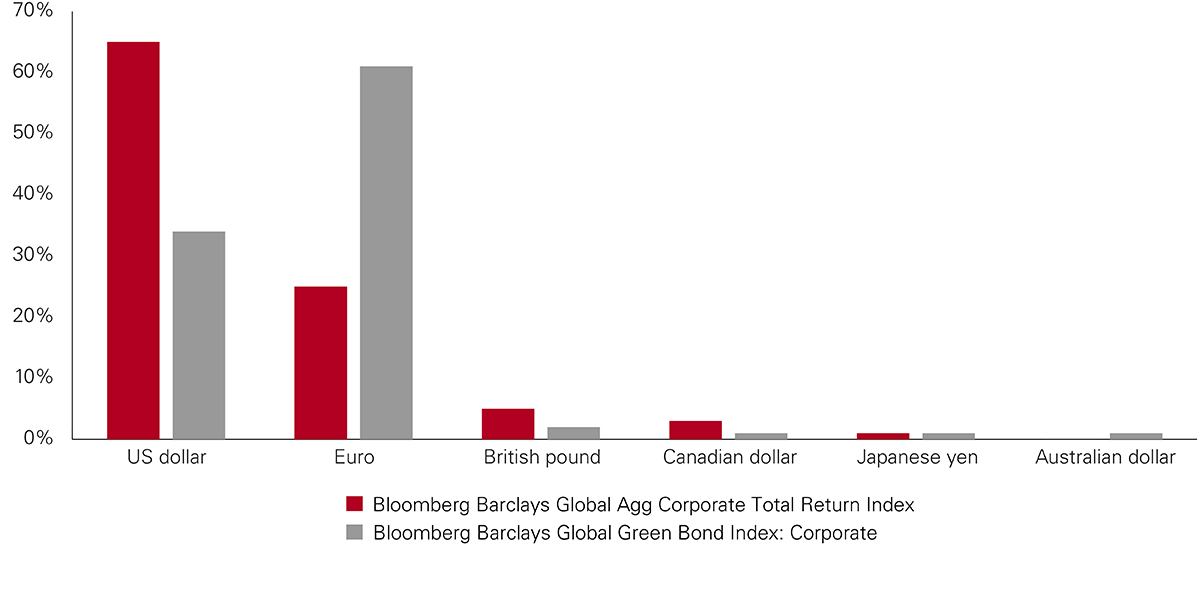

And while the green-bond market is rapidly expanding, diversification remains relatively low, particularly among corporate bonds. For example, the Bloomberg Barclays MSCI Global Green Bond Corporate Bond Index includes bonds across eight currencies and 16 sectors. By contrast, the Bloomberg Barclays Global Aggregate Corporate Bond Index comprises bonds spanning 13 currencies and 20 sectors8. The green bond index is also relatively concentrated among a small group of leading issuers, with the top-10 names making up 42%, 40% and 83% of the value of the USD, EUR and GBP sub-indices respectively9.

Bloomberg Barclays Global Aggregate Corporate Bond Index and Bloomberg Barclays MSCI Global Green Bond Corporate Bond Index by currency and sector

Source: Bloomberg, as at 28 February 2021.

Given these outsize exposures to certain currencies, sectors and issuers relative to the broader market, fundamental credit research and analysis is crucial while the green bond universe continues to grow and become more diversified.

An evolving market – but questions remain around transparency and accountability

The green bonds space has experienced rapid growth, but it is still in its infancy relative to other fixed income sub-asset classes. As the market evolves, new regulation and advances in standardisation—such as the International Capital Market Association’s Green Bond Principles and the EU taxonomy of green economic activities and Green Bond Standard—will likely bring further transparency and accountability.

We apply our rigorous analytical approach to any bond, be it green or conventional. And for investors, focusing on keeping costs to a minimum, taking a long-term approach and being diversified apply just as much to green bonds as they do to any other type of investment. With green bonds forming a growing part of major indices, understanding the unique risks involved is pivotal to managing fixed income portfolios. We anticipate that green bonds will play an important role in debt markets going forward.

Related Links:

1 Source: International Capital Market Association, as at 28 February 2021.

2 Source: Bloomberg Barclays, as at 28 February 2021.

3 Source: Morgan Stanley Research, April 2021.

4 Source: Bloomberg Barclays, as at 28 February 2021.

5 Source: Bloomberg Barclays, as at 31 March 2021.

6 Source: Vanguard.

7 Source: Vanguard.

8 Source: Bloomberg Barclays, as at 28 February 2021.

9 Source: Bloomberg Barclays and Vanguard, as at 31 December 2020.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.

Investments in smaller companies may be more volatile than investments in well-established blue chip companies.

Reference in this document to specific securities should not be construed as a recommendation to buy or sell these securities, but is included for the purposes of illustration only.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

The Vanguard Emerging Markets Bond Fund and Vanguard Global Credit Bond Fund, may use derivatives, including for investment purposes, in order to reduce risk or cost and/or generate extra income or growth. For all other funds they will be used to reduce risk or cost and/or generate extra income or growth. The use of derivatives could increase or reduce exposure to underlying assets and result in greater fluctuations of the Funds net asset value. A derivative is a financial contract whose value is based on the value of a financial asset (such as a share, bond, or currency) or a market index.

Some funds invest in securities which are denominated in different currencies. Movements in currency exchange rates can affect the return of investments.

For further information on risks please see the “Risk Factors” section of the prospectus on our website at https://global.vanguard.com.

Important information

This is an advertising document.

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

Vanguard Investment Series plc has been authorised by the Central Bank of Ireland as a UCITS and has been registered for public distribution in certain EEA countries and the UK. Prospective investors are referred to the Funds' prospectus for further information. Prospective investors are also urged to consult their own professional advisers on the implications of making an investment in, and holding or disposing shares of the Funds and the receipt of distributions with respect to such shares under the law of the countries in which they are liable to taxation.

The Manager of Vanguard Investment Series plc is Vanguard Group (Ireland) Limited. Vanguard Asset Management, Limited is a distributor of Vanguard Investment Series plc.

For further information on the fund's investment policies, please refer to the Key Investor Information Document (“KIIDs”). The KIID for this fund is available in local languages, alongside the prospectus via Vanguard’s website https://global.vanguard.com/.

The funds or securities referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds or securities. The prospectus or the Statement of Additional Information contains a more detailed description of the limited relationship MSCI has with Vanguard and any related funds.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. BARCLAYS® is a trademark and service mark of Barclays Bank Plc, used under license. Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited ("BISL") (collectively, "Bloomberg"), or Bloomberg's licensors own all proprietary rights in the Bloomberg Barclays Indices.

The products are not sponsored, endorsed, issued, sold or promoted by “Bloomberg or Barclays”. Bloomberg and Barclays make no representation or warranty, express or implied, to the owners or purchasers of the products or any member of the public regarding the advisability of investing in securities generally or in the products particularly or the ability of the Bloomberg Barclays Indices to track general bond market performance. Neither Bloomberg nor Barclays has passed on the legality or suitability of the products with respect to any person or entity. Bloomberg’s only relationship to Vanguard and the products are the licensing of the Bloomberg Barclays Indices which are determined, composed and calculated by BISL without regard to Vanguard or the products or any owners or purchasers of the products. Bloomberg has no obligation to take the needs of the products or the owners of the products into consideration in determining, composing or calculating the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays is responsible for and has not participated in the determination of the timing of, prices at, or quantities of the products to be issued. Neither Bloomberg nor Barclays has any obligation or liability in connection with the administration, marketing or trading of the products.

For Dutch investors only: The fund(s) referred to in this document are listed in the AFM register as defined in section 1:107 Dutch Financial Supervision Act (Wet op het financieel toezicht).For details of the Risk indicator for each fund listed in this document, please see the fact sheet(s) which are available from Vanguard via our website https://www.vanguard.nl/portal/instl/nl/en/product.html.

For Swiss professional investors: The Manager of Vanguard Investment Series plc is Vanguard Group (Ireland) Limited. Vanguard Investments Switzerland GmbH is afinancial services provider, providing services in the form of purchase and sales according to Art. 3 (c)(1) FinSA. Vanguard Investments Switzerland GmbH will not perform any appropriateness or suitability assessment. Furthermore, Vanguard Investments Switzerland GmbH does not provide any services in the form of advice. Vanguard Investment Series plc has been authorised by the Central Bank of Ireland as a UCITS. Prospective investors are referred to the Funds' prospectus for further information. Prospective investors are also urged to consult their own professional advisors on the implications of making an investment in, and holding or disposing shares of the Funds and the receipt of distributions with respect to such shares under the law of the countries in which they are liable to taxation. Vanguard Investment Series plc has been approved for offer in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA). The information provided herein does not constitute an offer of Vanguard Investment Series plc in Switzerland pursuant to FinSA and its implementing ordinance. This is solely an advertisement pursuant to FinSA and its implementing ordinance for Vanguard Investment Series plc. The Representative and the Paying Agent in Switzerland is BNP Paribas Securities Services, Paris, succursale de Zurich, Selnaustrasse 16, 8002 Zurich. Copies of the Articles of Incorporation, KIID, Prospectus, Declaration of Trust, By-Laws, Annual Report and Semiannual Report for these funds can be obtained free of charge from the Swiss Representative or from Vanguard Investments Switzerland GmbH via our website https://global.vanguard.com/.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2021 Vanguard Group (Ireland) Limited. All rights reserved.

© 2021 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2021 Vanguard Asset Management, Limited. All rights reserved.

743