ETF knowledge centre

ARE YOU READY TO TAKE YOUR ETF KNOWLEDGE TO THE NEXT LEVEL?

An overview of exchange-traded product types

ETFs are part of a group of investments known as exchange-traded products (ETPs).

While there are many types of ETPs, all are investments that trade on an exchange and offer exposure to shares, bonds or other assets such as commodities.

ETFs make up the lion’s share of the ETP universe. Most ETFs seek to track a traditional market-capitalisation-weighted index, such as the S&P 500 or the Euro Stoxx 50. In recent years, an increasing number of active ETFs have become available. These include rules-based, alternatively weighted ETFs (often called smart beta or strategic beta strategies), which seek to track non-market-cap-weighted indices usually in an attempt to outperform the market or manage risk.

As at 30 November 2018 , there were more than 2,285 ETPs available in Europe, of which over 1,800 were ETFs1.

1Source: ETFGI.

What are index ETFs?

While there are over 1,800 ETFs available in Europe1, most of their assets are invested in traditional index-based ETFs.

Indexing is a passive investment strategy that attempts to track the returns of a specific market index as closely as possible by holding all or a representative selection of securities in the index.

Most ETFs aim to track market-cap-weighted indices and are available in an increasing number of styles and asset classes, including regional and global equity and fixed income markets. They range from products that invest in the widest coverage of the markets, to those that invest in specific industries.

Some style ETFs cover the growth and value spectrum, and others track certain market-capitalisation ranges. International ETFs cover the global markets and may offer exposure to a single country or region of the world. Finally, fixed income ETFs can cover a variety of duration, credit quality and maturity ranges.

Market capitalisation: The traditional weighting methodology

An index is a group of securities chosen to represent an unbiased view of the risk-reward attributes of a market or portion of a market. Vanguard believes that indices should be constructed according to the market capitalisation of the underlying constituents.

Weighting securities according to their market capitalisation is the most commonly used method. Market-cap-weighted indices reflect the consensus estimate of each company's value at any given moment. In any open market, new information – economic, financial or company-specific – affects the price of one or more securities and is reflected instantaneously in the index via the change in its market capitalisation.

1Source: ETFGI as at 30 November 2020.

How do index ETFs track their benchmarks?

Index ETFs use three primary strategies in an effort to track their benchmarks as closely and effectively as possible.

Full replication

The most common way to create an index portfolio is to fully replicate a target index by purchasing securities according to their relative weight in the index. This process helps ensure an ETF tightly tracks its index while closely matching key index characteristics. Full replication is typically used for concentrated indices with liquid constituents such as the S&P 500, Euro STOXX 50 or government bond indices.

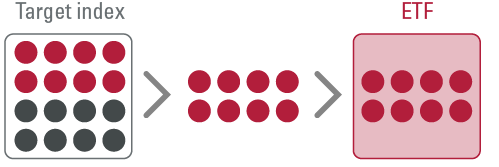

Sampling

The ETF holds a representative sample of the securities that make up the index. A sampling approach is used when there is a large number of holdings in the index, making full replication difficult and costly. The sample aims to match the essential characteristics of the index and to track its returns.

This strategy:

- Divides securities into small groups across a variety of key characteristics.

- Allows a security to be chosen by the portfolio manager from that small group and weighted according to the corresponding weight in the index.

- Can result in increased tracking differential.

Most bond index ETFs replicate their benchmarks through a sampling approach. Full replication for bond ETFs is often impractical due to the sheer number of issues in their target indices and the less liquid nature of some of the issues.

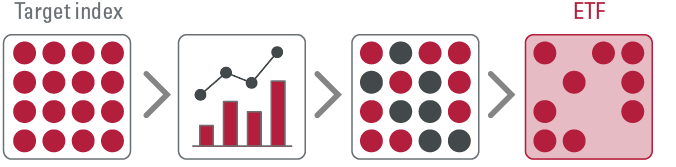

Optimisation

Rather than using a sample based on industry or security characteristics, this approach uses a quantitative multifactor model in an effort to track the index.

This strategy:

- Uses a computer model to determine the optimal portfolio composition based on historical price changes and correlation of securities within the index.

- Relies on historical data and factors that may change over time, which may result in greater tracking error, albeit at a generally lower cost.

Most equity ETFs tracking indices with lots of constituents, such as the FTSE All-World Index, replicate their benchmarks through optimisation.

What affects index tracking?

Tracking difference (sometimes referred to as excess return) and tracking error are important metrics to consider, especially when evaluating traditional index-based ETFs.

Understanding what they measure can help you make smarter investment decisions.

Tracking difference for index ETFs

Tracking difference measures an ETF's performance against its benchmark index over a specific period of time. Calculating tracking difference is fairly simple: Subtract the index's total return from the ETF's total return.

Tracking difference can be positive or negative and reveals the extent to which an ETF outperforms or underperforms its benchmark index.

Tracking error

ETF providers define tracking error in different ways. The formal definition of tracking error is the annualised standard deviation of tracking difference. In other words, while tracking difference measures the amount by which an ETF's return differs from that of its benchmark over a specified period, tracking error measures the variability of tracking difference over time.

For example, if the tracking error is 50 basis points, about two-thirds of the time the ETF’s excess returns are expected to be within 50 basis points of the average excess return. A lower tracking error would suggest lower variability of the excess return.

We believe that if your primary objective is seeking total return over a long-term time frame, then excess return is a more important measure than tracking error. However, over the short term, you may care more about performance consistency and want to minimise volatility, in which case you may wish to focus on tracking error.

In the hypothetical example shown here, investors seeking stronger long-term returns may find Fund A the better choice, despite its higher tracking error. However, investors who value returns that don't deviate too far from the benchmark may be attracted to Fund B, despite its lower average returns (i.e. greater negative tracking error).

![]()

When comparing funds in real life, you might not find such a clear-cut trade-off between tracking difference and tracking error. Other factors, such as asset allocation, index methodology and cost should also be evaluated before selecting an investment.

Key causes of tracking error and tracking difference

In an ideal world, ETFs would perfectly track their benchmark indices, and tracking difference and tracking error would not exist. However, from a practical standpoint, a number of factors work to make that ideal impossible to achieve.

Fees

By creating a drag on performance, fees are the most common contributor to negative tracking difference. Be sure to evaluate all of a fund's fees, including the trading costs, which are not included in the ongoing charges figure/total expense ratio (OCF/TER). Swap fees associated with synthetic ETFs are also not included in the OCF/TER. They can vary over time and consequently can be an important cause of tracking error and tracking difference.

Management expertise

A good index fund manager will understand when to use a full replication approach and when a sampling or optimisation approach may be more appropriate. A manager must also be adept at handling index constituent changes, index reconstitutions, fund cash flows and more.

Replication methodology

Replication methodology can be a major contributor to both tracking error and tracking difference. Fully replicated ETFs tend to have lower tracking errors than optimised and sampled ETFs.

Taxation

Depending on the domicile of the ETF, there may be withholding taxes both on dividends in the underlying portfolio and also on distributions of the ETF itself. Those taxes should be considered when analysing and comparing the performance of ETFs. Withholding taxes on dividends in the underlying portfolio are reflected in the ETF’s net asset value. As a result, they also have a direct impact on an ETF’s performance and any tracking difference.

What are the potential benefits of indexing?

Traditional index investing – through market-cap-weighted ETFs or mutual funds – can offer several significant benefits.

Low costs

Index funds have a powerful advantage over most actively managed funds – lower costs. Here are two main reasons:

- Lower management costs. It simply costs less to manage and operate an index fund. That's because index funds don't have to employ highly paid teams to analyse and select securities.

- Lower transaction costs. Index funds use a buy-and-hold approach, which means that index fund managers generally trade securities less often than active fund managers. Less trading reduces brokerage commissions and other expenses associated with trading securities.

Diversification

Maintaining a diversified portfolio is an essential part of a successful investment plan. Indexing can be a simple way to achieve diversification.

Competitive long-term performance

Thanks to their diversification and low costs, index funds can be an effective way to achieve competitive returns over the long run.

Transparency

Index funds have a precise, easily understood objective: to track the performance of a specific index (before fees and expenses). With index funds, you always know how your money is invested.

Low manager risk

Index funds reduce exposure to manager risk, which is the risk that poor security selection will cause underperformance. That's because they seek to track, not outperform, a market index. Active fund performance, on the other hand, is subject to more uncertainty.

Risks

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Investments in smaller companies may be more volatile than investments in well-established blue chip companies.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.

ETF shares can be bought or sold only through a broker. Investing in ETFs entails stockbroker commission and a bid-offer spread which should be considered fully before investing.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

The Funds may use derivatives in order to reduce risk or cost and/or generate extra income or growth. The use of derivatives could increase or reduce exposure to underlying assets and result in greater fluctuations of the Fund's net asset value. A derivative is a financial contract whose value is based on the value of a financial asset (such as a share, bond, or currency) or a market index.

Some funds invest in securities which are denominated in different currencies. Movements in currency exchange rates can affect the return of investments.

For further information on risks please see the “Risk Factors” section of the prospectus on our website at https://global.vanguard.com.

What are the different types of ETFs?

While there are over 1,800 ETFs available in Europe today,1 most of their assets are invested in traditional index-based ETFs.

Index ETFs

The goal of an index ETF is to track the performance of a specific market benchmark as closely as possible. Examples of well-known benchmarks are FTSE 100, Euro STOXX 50 or S&P 500. That's why you may hear it referred to as a "passively managed" investment.

Index-based ETFs are available in an increasing number of styles and asset classes, including regional and global equity and fixed income markets. They range from products that invest in the widest coverage of the markets, to those that invest in specific industries.

Some style of ETFs cover the growth and value spectrum, and others track certain market-capitalisation ranges. International ETFs cover the global markets and offer exposure to a single country or region of the world. Finally, fixed income ETFs cover a variety of duration, credit quality and maturity ranges.

1Source: ETFGI as at 30 November 2020.

Other types of ETFs

A recent surge of interest in ETFs has led to significant product innovation. The latest global industry offerings include ETFs that go beyond a traditional index-based approach.

Actively managed ETFs

Rather than aiming to closely track a market index, the portfolio manager actively manages the assets within the ETF to achieve a particular investment objective. Actively managed ETFs represent a small but growing portion of the overall industry.

Commodity and currency ETFs

These ETFs invest in the commodities and currency markets either through physical assets or through the futures markets. They provide investors with exposure to alternative investments such as agricultural products, precious metals, energy and currencies.

Inverse and leveraged ETFs

Inverse and leveraged ETFs are types of synthetic ETFs. Inverse ETFs attempt to deliver the opposite, or inverse, returns of the benchmarks they track. An inverse ETF is expected to deliver a positive return on a day when its index goes down and a negative return when the index goes up.

Leveraged ETFs attempt to deliver multiples of the returns of the benchmarks they track. Such an ETF might be designed to return two or three times the value of the daily benchmark increase or, conversely, two or three times the benchmark's decline.

It's important to remember that most inverse and leveraged ETFs are designed to achieve their objectives daily. When held for more than a day, these ETFs can produce returns that differ from the inverse or leveraged multiple. Inverse and leveraged ETFs are generally appropriate for an extremely narrow set of investment objectives – such as for short-term market timing or hedging purposes – and are not intended for long-term investment.

Replication Methodology

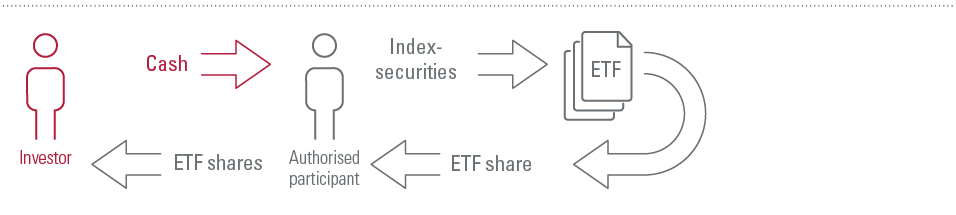

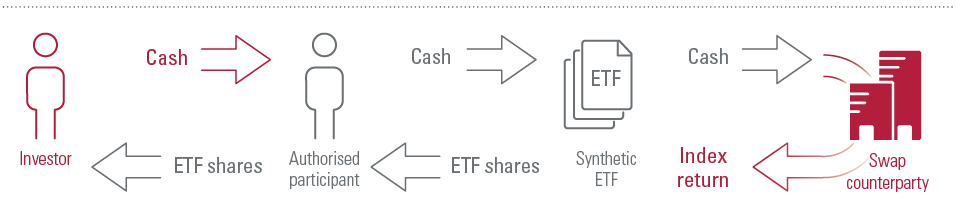

ETFs can be classified as physical or synthetic depending on the nature of their underlying holdings.

Most ETFs are classified as physical because they hold the actual securities that make up their underlying portfolios. All Vanguard ETFs are physically replicated. Synthetic ETFs rely on derivatives, mainly swaps, to execute their investment strategy.

Swaps are agreements between the ETF and a counterparty – usually a bank – to pay the ETF the return of its index. In essence, a synthetic ETF can track an index without actually owning any of its securities.

Though synthetic ETFs are available in many markets, they are most popular in Europe, where they were introduced in 2001. That said, there is a growing preference among investors for physical ETFs.

How physical and synthetic ETFs work

Physical ETF

Synthetic ETF

Comparing physical and synthetic ETF structures

| Physical ETFs | Synthetic ETFs | |

|---|---|---|

| Underlying holdings | Physical securities from underlying index | Derivatives/swaps and collateral basket (different from index in most cases) Collateral and/or swaps |

| Transparency | Yes | Limited (e.g. swap fees, collateral basket) |

| Counterparty risk | Limited (securities lending), always fully collateralised | Yes (derivatives/swaps), often collateralised |

| Sources of costs | Expense ratio, rebalancing costs | Expense ratio plus swap fee |

Source: Vanguard

Counterparty risk

One of the main risks of synthetic ETFs is counterparty risk. Essentially, synthetic ETF investors trust that the total-returns swap provider will meet its obligation to pay the agreed-upon index return. If that doesn't happen, investors risk incurring a loss. The key risk mitigator in the event of a counterparty default is collateral.

Physical ETFs are also exposed to counterparty risk through any securities lending programme. This activity, however, is always fully collateralised to protect investor assets.

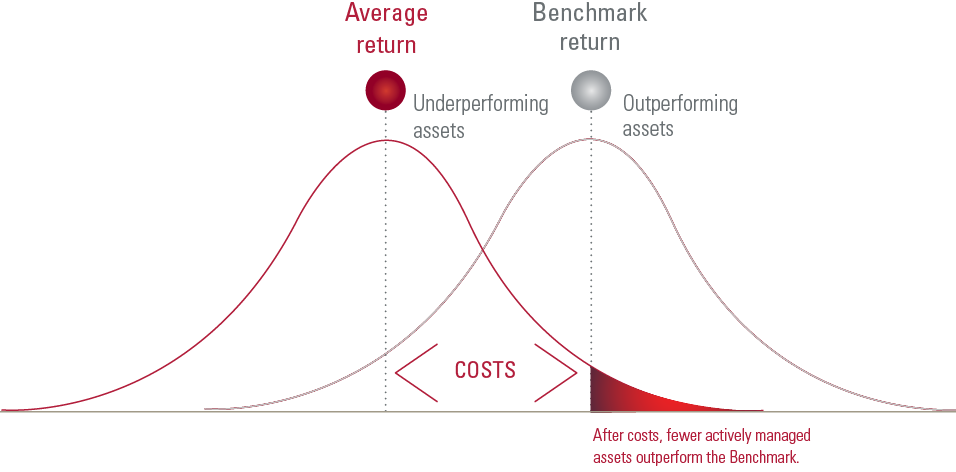

Why do investment costs matter?

Investment costs are a key driver of long-term performance.

The zero-sum game helps explain why. The theory states that the aggregate holdings of all investors in a particular market form that market. At any time, half of invested assets must outperform the average market return and the other half must underperform it. Once costs are subtracted, though, it becomes increasingly difficult to beat the average market return. This graphic helps tell the story.

Source: Vanguard

The zero-sum game provides a theoretical explanation for why costs are such an important influence on returns. It makes a case for keeping costs low, regardless of whether you choose an index or active strategy.

But it’s more than just theory. Research by Vanguard and others shows that what an investor pays for an investment can affect their net returns more than anything else1.

1Vanguard, 2017. Vanguard’s Principles for Investing Success. Valley Forge, Pa.: The Vanguard Group.

What are active ETFs and how do they work?

Actively managed ETFs are a relatively new category of exchange-traded product.

They offer the opportunity for market outperformance, but come with the potential trade-offs of higher costs, greater tracking error and risk of underperforming the market.

Like other exchange-traded products, active ETFs trade on an exchange and are open-ended. Ongoing costs are generally lower than traditional actively managed funds, but higher than traditional index funds and ETFs.

Types of active ETFs

Alternative index ETFs

Commonly referred to as smart beta or strategic beta ETFs, these products seek to track alternatively weighted, rules-based indices, with the goal of outperforming market-cap-weighted indices. Factor tilts, for example toward value or small company shares, often explain the performance of these products relative to the broad market. (See the callout to learn more about factors).

Alternatively weighted index products blur the line between active and passive management. They are index based, yet the construction of their benchmarks reflects an active decision to deviate from market-cap weightings.

Active factor ETFs

The managers of these products seek to explicitly target a factor, or combination of factors, that they believe will deliver an investment premium such as outperformance or reduced volatility. (See the callout to learn more about factors).

Active factor ETFs don’t track a benchmark. Not being tied to an index rebalancing schedule gives the manager the flexibility to add or reduce positions as needed to maintain exposure to the desired factors. Active factor ETFs typically use a quantitative, rules-based security selection process to build their portfolios.

Comparing management approaches

ETFs can differ greatly when it comes to the management of their underlying portfolios.

| Index-based | Market-cap-weighted | Rules-based management | Active management | Active risk | |

|---|---|---|---|---|---|

| Traditional index ETFs | |||||

| Alternative index ETFs (e.g. "smart beta") | |||||

| Active factor ETFs |

What are factors?

One way to think about factors is as the DNA of an investment. They are underlying attributes that explain and influence how an investment behaves. By targeting these attributes, factor-based investments attempt to deliver an investment premium, such as market outperformance or reduced volatility.

One factor you’re probably familiar with is the market factor. Also known as equity risk, the market factor shapes and explains the risk and returns of a market-capitalisation-weighted equity portfolio. Historically, a portfolio exposed to the market factor has outperformed “risk-free” investments such as short-term government bonds. This return premium has been an investor’s reward for bearing the additional risks of equity investing. Other well-known equity factors include value, size and momentum.

Many investors’ portfolios tilt toward certain factors and away from others, whether they know it or not. These tilts explain much of the risk and returns across a range of investments, including smart/strategic beta ETFs, active factor ETFs, and traditional active funds.

Basics

Learn the basics of ETFs, including their history, how they compare to mutual funds and more.

Trading

Learn how ETFs trade, where they get liquidity, common order types, how premiums and discounts work and more.

Strategies

Learn about strategic and tactical uses for ETFs, including portfolio completion, liquidity management and more.